This guidance is part of a comprehensive set of guidelines issued recently by the Central Board of Direct Taxes (CBDT) for compulsory selection of Income-tax (I-T) returns for the purpose of complete scrutiny.

These guidelines, which are issued annually, pertain to the selection and complete scrutiny that is to be undertaken during the current financial year 2024-25 and cover survey cases, search and seizure cases, tax evasion cases, cases where no I-T return was filed in response to an inquiry notice under section 142(1).

It also covers cases relating to non-registration or cancellation of registration under various sections – such as 12A/12AB relating to registration of charitable organizations to be eligible for tax benefit. In addition, if in an earlier year, an addition was made to the taxpayers’ income on a recurring issue, then subject to monetary limits that have been laid down, the I-T return will be picked up under compulsory scrutiny guidelines. The guidelines also prescribe the role and responsibilities of the I-T officers and the National Faceless Assessment Centre (NFAC).

According to Ketan Vajani, chartered accountant, there is no significant change in the criteria for compulsory scrutiny as compared to the present position. “The guideline points out that all I-T returns filed during financial year 2023-24, will have the outer time limit for issue of a notice by June 30, 2024. This is pursuant to the amendment carried out by Finance Act, 2021, which has reduced the time limit for service of notice under section 143(2) to three months from the end of the financial year in which the return is filed.”

Complete scrutiny is a regular feature carried out in selective cases to ascertain whether the taxpayer has declared income correctly in the I-T returns and has paid the taxes due. Complete scrutiny which is to be carried out during the current financial year, covers cases of tax evasion, where specific information in this regard has been provided by any law enforcement agency – including the I-T department’s own investigation wing and a I-T return has been filed by the taxpayer. Complete scrutiny will enable the I-T officer to know the income that has not been declared in the I-T returns (escaped assessment).

Improved technology which enables easier sharing of information between government agencies and also information from other countries, has made it easier for I-T officials to zoom down on such cases. “However, tax tribunals have in many cases, nullified reassessment orders, if the I-T officers have blindly relied on investigative reports of various agencies, without carrying out due diligence,” points out Vajani.

Related Posts

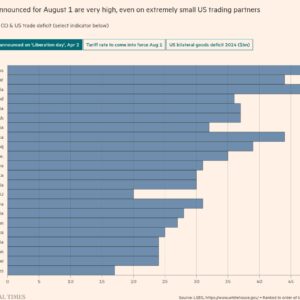

A return to tariffs, Taco or not

Unlock the White House Watch newsletter for free Your guide to what Trump’s second term means for Washington, business and the world Like a dog to a bone, Donald Trump…

Read more

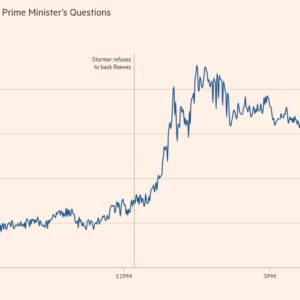

Starmer moves to bolster Reeves after tearful Commons episode fuels bonds slump

Unlock the Editor’s Digest for free Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter. Sir Keir Starmer has said Rachel Reeves will be chancellor…

Read more

US halts some weapons deliveries to Ukraine

Unlock the White House Watch newsletter for free Your guide to what Trump’s second term means for Washington, business and the world The White House has abruptly halted shipments of…

Read more

US banks announce big shareholder payouts as Fed eases stress tests

Stay informed with free updates Simply sign up to the US banks myFT Digest — delivered directly to your inbox. Investors reaped the rewards of looser bank supervision as Wall…

Read more

Eurozone inflation rises to ECB’s 2% target

Unlock the Editor’s Digest for free Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter. Eurozone inflation hit 2 per cent in June, rising back…

Read more

Revised UK welfare reforms to push 150,000 into poverty

Unlock the Editor’s Digest for free Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter. Watering down the government’s flagship welfare changes will cost taxpayers…

Read more